Real Estate Investment Strategies

DSCR or Debt-Service Coverage Ratio loans enable real estate investors to qualify based on rental income generated rather than personal income. These loans are ideal for self-employed investors, investors with multiple mortgaged rental properties, and investors looking to grow their portfolios rapidly. Let's take a closer look at:

The debt-service coverage ratio (DSCR) is a measure of the cash flow available to pay current debt obligations.

DSCR is used to analyze firms, projects, or individual borrowers.

The minimum DSCR that a lender demands depends on macroeconomic conditions. If the economy is growing, lenders may be more forgiving of lower ratios.

A DSCR calculation greater than 1.0 indicates there is barely enough operating income to cover annual debt obligations, while a calculation less than one indicates potential solvency problems.

While the interest coverage ratio calculates the ability to meet interest payments, DSCR incorporate principal obligations.

What is a DSCR Loan?

Unlike a consumer or owner-occupied mortgage loan, but similar to a commercial real estate mortgage, a DSCR loan is underwritten based on property-level cash flow, rather than personal income. DSCR or Debt-Service Coverage ratio is a tool to help lenders understand a borrower's ability to pay back a loan based on the monthly rental income of the property. DSCR is a simplified way to measure cash flow and is calculated by dividing the monthly rent by the monthly principal and interest payments, taxes, insurance, and association dues (PITIA).

DSCR Loan Property Types

DSCR loans typically can be used for the following property types:

Single-family (1-4 unit) residential

Vacation or short-term rentals

Commercial or multifamily property

DSCR loans typically cannot be used for the following property types:

Rural properties

Properties with square footage of less than 750 square feet

Condotels

Manufactured housing

Dome homes

Log cabins

Why are DSCR Loans Significant to Investors?

Also referred to as investment property loans, Non-QM loans, and rental loans, among other synonyms, DSCR loans have become quite trendy recently. So what is all the buzz about? While it is possible for investors to obtain a

or funds through a small bank, this financing is tedious to qualify for and has substantial liquid reserve requirements. DSCR Loans, on the other hand, are specifically designed for the professional investor. Let's take a closer look.

DSCR Loans are Underwritten Based on Gross Rental Income Instead of Personal Financial History

Experienced real estate investors with multiple mortgaged investment properties and self-employed investors without W2's often have difficulty meeting conventional loan criteria. The credit, reserve, and income requirements of conventional loans are strenuous. Further, they are underwritten using Debt-to-Income ratio or DTI, which looks at your personal income compared to your personal debt. If you are trying to finance the purchase of a rental property with a conventional loan, the payment for the new loan will be included in the debt portion of your debt-to-income calculation. Whether you can offset that new monthly payment with a portion of the expected rent on the new investment property will depend on how well you can document the actual or expected rents from the property.

Investors that have a lot of personal income from non-investment property sources, may be able to cover the “cash flow gap” on their DTI calculation up to some point. Investors that are self-employed or have a lot of investment properties may not have income from other sources to cover this gap. Using debt service coverage ratio eliminates DTI from the underwriting and instead focuses on the rental income from the subject property relative to the investment property related expenses.

DSCR Loans Allow Investors to Borrow in an LLC or Entity

M

any experienced investors prefer to borrow through an LLC or corporation to protect their identity and other investments. This adds an extra layer of protection to the investor's personal assets for any unfortunate incidents on the property. Conventional loans can only be obtained in an individual(s) name.

Most DSCR Lenders have more flexible common sense limitations on the maximum number of properties financed

Even if an investor has enough personal income to support multiple mortgaged rentals, with conventional loans you are maxed out at ten loans. Most DSCR lenders do not have set limits but instead use common sense when evaluating an investor's maximum credit exposure.

DSCR loans require less documentation

When applying for a conventional mortgage, you have to gather all of your pay stubs, bank and asset statements, and tax documentation. The underwriters are going to dive deep into your personal financial documents and history, which is time consuming and tedious. Any missing documentation or schedules in your tax returns can lead to lengthy delays. DSCR lenders focus on the value of the property and the expected cash flow of the property, plus the quality and depth of your credit. Most DSCR lenders will not ask you for documentation to verify your employment, income or assets (beyond required liquid reserves).

A Closer Look at How DSCR Loans Work

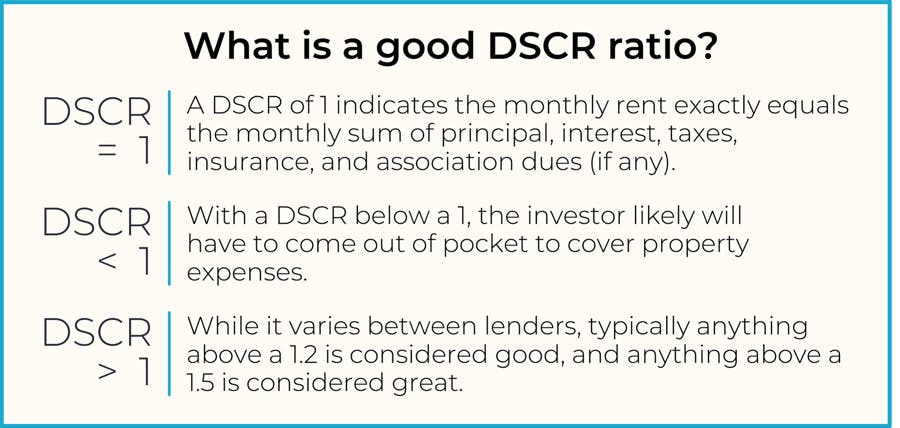

What makes a good Debt Service Coverage Ratio?

A debt service coverage ratio of 1.2 is solid , and anything above a 1.5 is strong. A DSCR ratio of 1 indicates the rent exactly equals the monthly sum of principal, interest, taxes, insurance, and association dues (if any). With a debt service coverage ratio below a 1, the investor will be subsidizing the PITIA with cash from other sources.

Let's look at some examples for a clearer picture.

DSCR Examples

DSCR < 1

Principal + Interest= $1,800

Taxes= $250

Insurance= $150

Association Dues=$35

Total PITIA= $2235

Rent= $2100

DSCR= Rent/PITIA=2100/2235=0.94

Since the DSCR is .94, we know the PITIA is greater than the monthly rent from the property, indicating negative cash flow.

DSCR =1

Principal + Interest= $1,500

Taxes= $350

Insurance= $150

Association Dues=$100

Total PITIA= $2100

Rent= $2100

DSCR= Rent/PITIA=2100/2100=1.0

Since the DSCR is 1.0, we know the PITIA is equal to the monthly property rent.

DSCR >1

Principal + Interest= $1,600

Taxes= $250

Insurance= $150

Association Dues=$35

Total PITIA= $2,035

Rent= $2350

DSCR= Rent/PITIA=2350/2035=1.15

If we divide the rent by PITIA, we get a DSCR of 1.15, which indicates positive cash flow.

DSCR Loan Requirements

If you are an investor and looking to obtain a DSCR mortgage, make sure you meet these basic requirements:

- - Minimum Credit Score Required: Most DSCR lenders require a 680 credit score with better rates for higher credit. Most lenders also have minimum tradeline requirements, including both amount and duration. Lenders also will consider whether you have any other significant credit events on your credit report, such as foreclosures, bankruptcies or past due payments.

- Minimum Down Payment or Equity: Maximum loan-to-value on purchase loans typically is 70%-80% and on refinances is 65%-75% depending on property type, credit and DSCR.

- Minimum Property Value: Most lenders have a minimum property value of $150k

What to Look for in a DSCR Lender

When comparing DSCR lenders, here are some considerations.

What are the lenders rate and fees?

It is important to know exactly what your costs will be for the loan. The last thing you want is to end up at the closing table with unexpected costs. Most lenders charge an origination fee and one or more administrative fees (underwriting fee, documentation fee).

What are the lenders eligible property types?

This may seem obvious, but it does vary between lenders. For instance, some lenders have DSCR Loan Programs for vacation rentals and others do not. Other common variations include warrantable vs. non-warrantable condos and multi-family vs. single-family homes.

Is the lender focused on and experienced in working with investors?

In our opinion, this is the most important consideration. Lenders who work with investors often understand the nuances associated with financing and have programs tailored to help investor needs. There are a lot of new DSCR lenders on the market. Here are some things you can look for to help hone in on the most experienced lenders:

- Ask about the numbers of DSCR loans they have closed

- Ask how long they have been offering and closing DSCR loans

- Ask whether they have a dedicated team of operations personnel that process and underwrite their DSCR loans

- Ask about their property insurance requirements, because they typically are materially different for investment properties as compared to owner-occupied properties

- Ask about their prepayment penalty or rate buy-down options. DSCR loans almost always have a prepayment penalty.

- Ask about the ability to finance in an LLC or corporate entity

Pros and Cons of DSCR Loans

DSCR loans are an option that have grown in popularity recently due to their use of rental income rather than personal income to evaluate whether you qualify or not. They are easier to qualify for than an agency or bank loan and are more cost-effective than

for financing an investment property. However, there are also drawbacks that should be considered when it comes to this type of loan.

Pros:

DSCR loans often have faster application and closing times without the need to submit personal financing documents.

There’s also more flexibility on the number of loans or properties, so scaling your business can be done more quickly if you can afford it.

Cons:

Typically, they require a higher down payment (often 15-25% of the property's value).

Interest rates and lender fees are also higher for a DSCR mortgage than a second home loan.

You’ll need to provide proof of experience in renting.

DSCR FAQs

DSCR loans are usually 150 bps to 300 bps higher than consumer rates. They tend to be higher because these loans are seen as higher risk than owner-occupied homes. For more information on latest rates and how DSCR rates are calculated, see our Investment Property Mortgage Rates page.

The simplest way to improve your DSCR ratio is to put more money down, however you can also shop insurance, fight property taxes annually, and charge more rent. Allowing pets or including upsells such as a washer and dryer are easy ways to add more to your rent.

In addition to credit score, DSCR is an indicator of a borrower's ability to pay back a loan based on the cash flow generated by the rental property.

A more accurate description for this loan program is a "Low DSCR Loan." Essentially, this product does use DSCR, but has additional qualifications. Many lenders, like REO Lending, offer No DSCR loans for investors in hot markets where the rents have not caught up with the property values.

Why You Should Partner with REO Lending for Your DSCR Loans

Financing DSCR loans requires specific expertise and differs from other loans in terms of:

Underwriting requirements: As an example, personal income history is not a consideration when underwriting DSCR loans.

Appraisal process: For a DSCR loan, an evaluation is needed of comparable rents in the area is needed in addition to the standard property appraisal report.

Borrower types: Often a real estate investor finances properties in an entity, which in itself has some lending nuances. For instance, there are necessary entity documents.

This is just a sampling of the many nuances associated with a DSCR mortgage. REO Lending has over a decade in mastering this niche market with over $2.1 billion in DSCR Loans originated, including over $641 million in vacation rentals.

Our DSCR Loan Features

Low documentation; no personal DTI, no tax returns;

- Full 30-year terms with no balloons; and

- The ability to protect your identity by financing through a corporate entity

- Common sense underwriting of your short-term rents